Pension reform has led to a number of new measures. During a webinar organized by Absoluce in partnership with Factorielles, company specializing in social protection advice for business leaders, Absoluce experts explained how it can modify the retirement strategies of employees and non-employees.

Several elements explain the difficulties in financing compulsory pensions. First of all, the duration of pension payment in France is the longest : it is paid for 22,2 years for men and 26,7 years for women. By comparison, durations in Europe are 19 to 20 years for men and 21 to 24 years for women. The employment rate for 60-64 year olds is 45% in Europe while it is only 33% in France. And finally, today in France, we leave on average a year earlier (62,8 ans) that 40 years ago, while for the same period, life expectancy has increased by more than seven years. Consequently, the replacement rates for pensions provided by compulsory schemes will continue to fall. The reform aims to increase the activity rate of seniors. The objective is for the employment rate of 60-64 year olds to reach 40% by the end of the decade. For that, a coercive measure is introduced, namely the postponement of the legal age from 62 to 64 years, and two incentive measures, namely the encouragement of combined employment and retirement and progressive retirement.

Individual solutions and collective solutions

In the future, maintaining your standard of living in retirement will require the subscription of additional plans. But many solutions are also possible to strengthen your retirement level. To meet the objective of maintaining standard of living in retirement, many devices are possible :

– individual solutions : real estate, stock savings plan, ordinary securities account, life insurance, capitalization contracts ;

– collective solutions : retirement savings plans (Individual PER and company PER), company savings plan. This pension reform opens up perspectives that require surrounding yourself with expert advice. The more we anticipate, the more levers you have to optimize your retirement. Strategies also differ depending on whether people are single or in a relationship. And finally, It is strongly recommended that you regularly review your strategy in this area throughout your working career..

The discount will be less severe with the reform

For the record, the maximum retirement liquidation rate is set at 50% of gross average annual income, limited to PASS (annual Social Security ceiling, or 43,992 euros in 2023). It is called full rate. Before the reform, if an individual retired at age 62, he was missing 20 quarters compared to the age of 67 when he automatically had his full rate. Taking into account the discount of 0,625% per missing quarter, this took away 12,50 %. 50 % – 12,50% = his pension rate was 37,50 %. With the reform, the age is still 67, but the discount only applies from age 64. With the same calculation rule, we arrive at a discount limited to 7,5 %. The pension rate will therefore be 42,50 % (50 % – 7,5 %).

Buying back quarters can become interesting

Quarterly buybacks were presented during the Fillon reform as being very interesting thanks to a leverage effect. If you want to retire early, you must have acquired all these trimesters. It is possible to buy back 12 “basic” quarters without the supplement. Previously, notably with the Agirc-Arrco regime, a penalty penalized people who, at 62 years old, had to wait a year to benefit from their full supplementary pension. From now on, the redemption of quarters will trigger the liquidation of the supplementary pension without discount. Au 1er avril 2024, all people who “suffered” a penalty will no longer suffer it. This buy-back of quarters can be all the more interesting if the retiree wants to continue working in combination with retirement employment..

Quarterly buybacks were presented during the Fillon reform as being very interesting thanks to a leverage effect. If you want to retire early, you must have acquired all these trimesters. It is possible to buy back 12 “basic” quarters without the supplement. Previously, notably with the Agirc-Arrco regime, a penalty penalized people who, at 62 years old, had to wait a year to benefit from their full supplementary pension. From now on, the redemption of quarters will trigger the liquidation of the supplementary pension without discount. Au 1er avril 2024, all people who “suffered” a penalty will no longer suffer it. This buy-back of quarters can be all the more interesting if the retiree wants to continue working in combination with retirement employment..

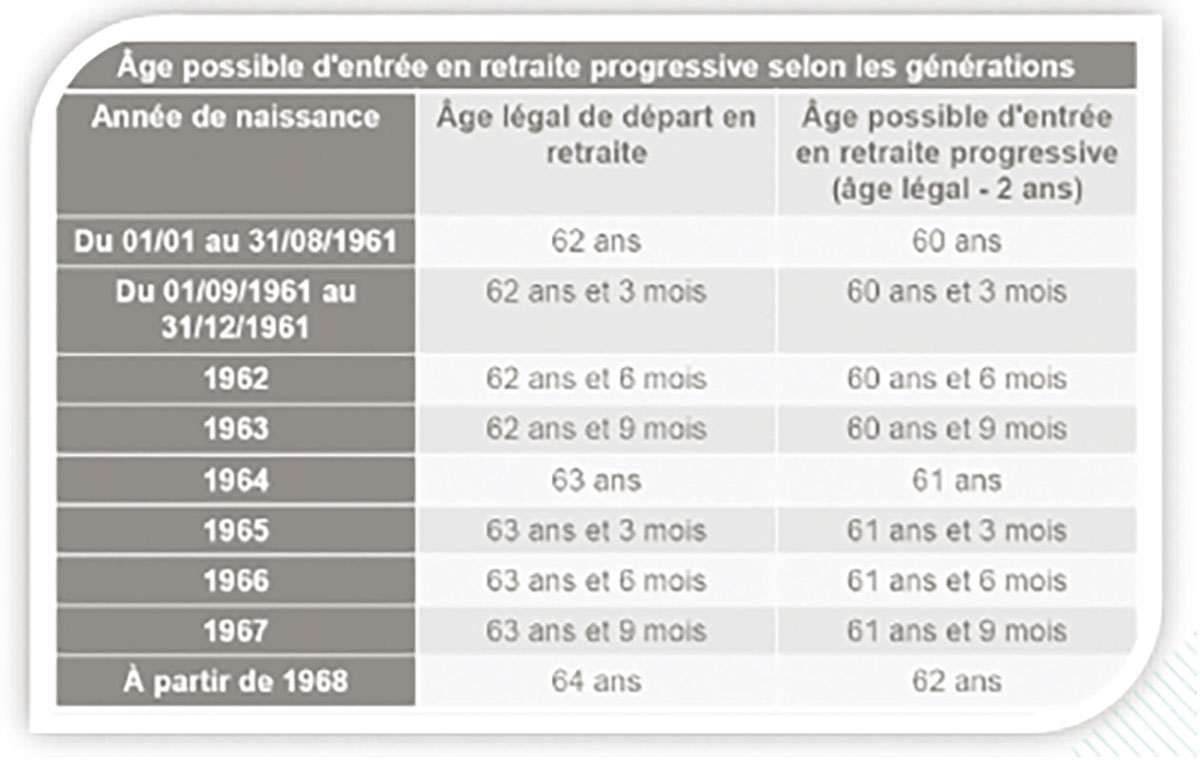

Take advantage of the opening of gradual retirement

Gradual retirement allows you to combine part-time work and the benefit of part of your retirement pension. This device, often overlooked, was previously reserved for private sector employees. It had recently been opened to executives on a day package and to corporate officers. The reform went even further by extending it to liberal professions (including lawyers) and civil servants. The rule has not changed : it is possible to benefit from progressive retirement two years before the legal retirement age. With the postponement of the retirement age to 67, the age at which it is possible to enter the system is modified (see table). The system is very interesting, but has not had much success until then. It is not certain that there will be more in the future... In addition to part-time and consequently the limitation of income, the employee must agree. It is interesting for the transmission of know-how, but in a small business it may be more complicated.

The accumulation of employment and retirement gives the right to a second pension

To benefit from this device, you must have reached the minimum legal age, have your full retirement. And liquidate all your pensions at the same time. For employees only, you must have stopped your previous activity, and respect a waiting period of six months if they return to work for the same employer. Two systems coexist : cumulative retirement employment capped (income from the new activity cannot exceed a certain ceiling) and liberalized retirement and employment accumulation (which allows the income from the new activity to be fully combined with the retirement pension). So far, working in combination with retirement did not allow you to build up new retirement rights. From now on, policyholders with multiple employment liberalized pensions acquire pension rights on the activity continued or resumed. The new pension will be calculated using only the contributed periods. (redemptions of contributions excluded) with application of the full rate. Its amount is capped at 5% of the PASS, is, in 2023, 183,30 euros per month. After liquidation of a second pension, a new activity will not give rise to another pension (no third pension).

Self-employed workers with combined employment and retirement will have a choice to make

TNS have two options : either they take remuneration from their “new” activity, and in this case this is subject to social charges and gives rights to a second retirement - but for 183,80 euros maximums —, either they choose the status of president of SAS and can in this case pay themselves dividends, but which do not give rise to a second pension.

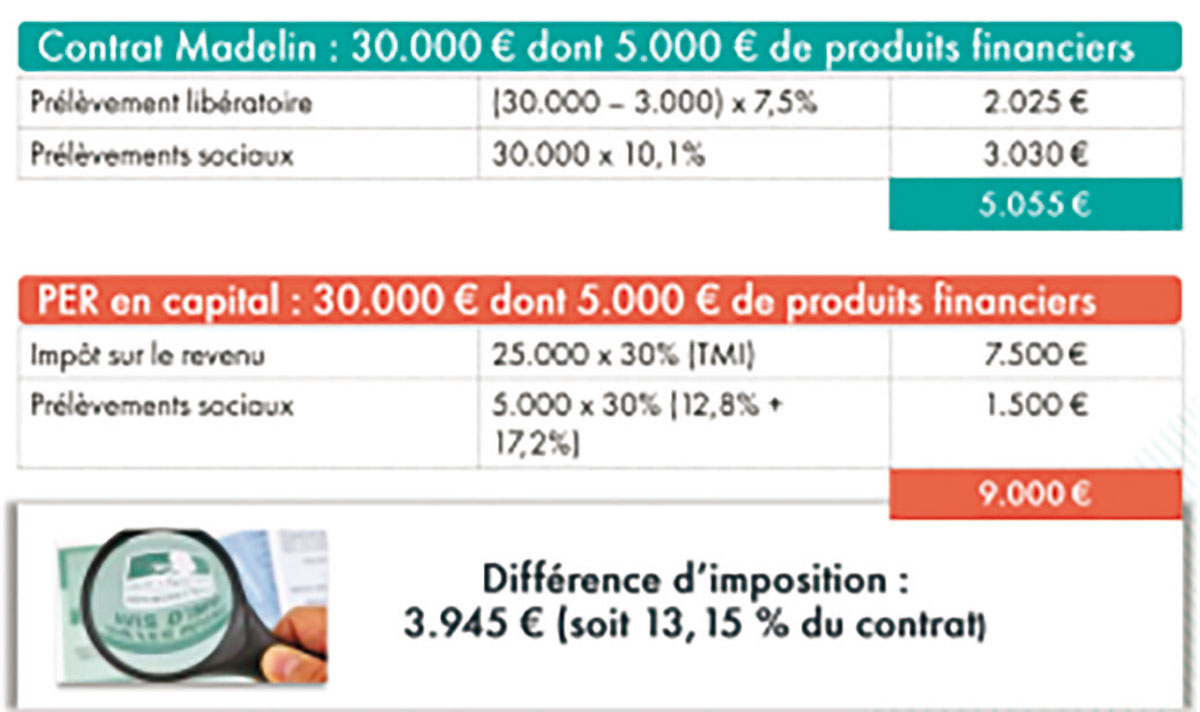

PER : better several small contracts in different companies

For old contracts, previously, capital exit was an option. From now on, to support the purchasing power of small savers, if the pension amounts to up to 110 euros per month, subscribers can demand the capital outflow. otherwise, From now on, it is the subscriber who chooses whether he wants to take out an annuity or capital. The insurer can no longer impose an option, he must ask her opinion. And his choice is no longer irrevocable. The subscriber can choose to take out an annuity, while being able to change your mind and request the exit of the remaining capital a few years later. When a subscriber has several contracts of a small amount within the same company, it is the total amount of all these small contracts which is taken into account. When you take out several contracts, it is therefore preferable to subscribe to them in different companies ; this will offer more flexibility to the subscriber. However, be careful with taxation. Taking into account the taxation on one side of Madelin contracts, PERP et article 83, and on the other side of the PER in capital, subscribers have no interest in transferring the former to the latter. If they want a capital exit, small subscribers have every interest in keeping their small contracts and only subscribing to a PER when they approach the threshold which will no longer allow them to withdraw capital.

{kind=link}